A Guide to Cooperative Funding and Financing

You’ve chosen the cooperative model because it reflects your community’s values — shared ownership, power and benefits. Now, it’s time to make your vision a reality by securing capital.

While co-ops operate outside traditional lending structures, they work within a powerful, purpose-built financing ecosystem designed specifically for member-owned enterprises. Mission‑driven lenders, federal programs and cooperative development funds form a network that helps founders, nonprofit leaders and community organizers move from uncertainty to action.

The Cooperative Advantage — Unique Strengths in Securing Funding

Member-owned businesses, from agricultural producer cooperatives to worker-owned enterprises, have specific attributes that make them attractive to funders, particularly those with impact-oriented mandates. Democratic member control, deep-rooted community involvement and a focus on long-term stability set them apart from traditional businesses. These attributes appeal to lenders and grantmakers who prioritize sustainable economic development over quick returns.

Evolving policy explores the socioeconomic benefits of this model, influencing funding trends at the federal and state levels. As governments and foundations increasingly prioritize inclusive economic development, co-op grants and co-op community grants are within reach of organizations that prove community impact alongside financial viability.

These inherent advantages, including long-term stability and community focus, strengthen your position with mission-aligned funders.

What Are the Capital Sources?

Three primary categories of capital each serve distinct purposes. You can build a comprehensive plan by understanding how these sources work together.

- Member equity and investment: Direct contributions through share purchases and member loans form the foundation and demonstrate your commitment to external funders.

- Debt financing: Borrowed capital from banks, credit unions or specialized lenders provides growth capital, which you must repay with interest.

- Grant funding: Non-dilutive awards from government agencies and foundations support specific projects without requiring repayment.

Building Your Foundation With Member Equity and Investment

Member investment is the foundation of any cooperative. It signals to outside funders that your organization has an engaged, committed ownership base. But not all member capital works the same way. Co‑ops typically rely on two types of member financing — equity and debt.

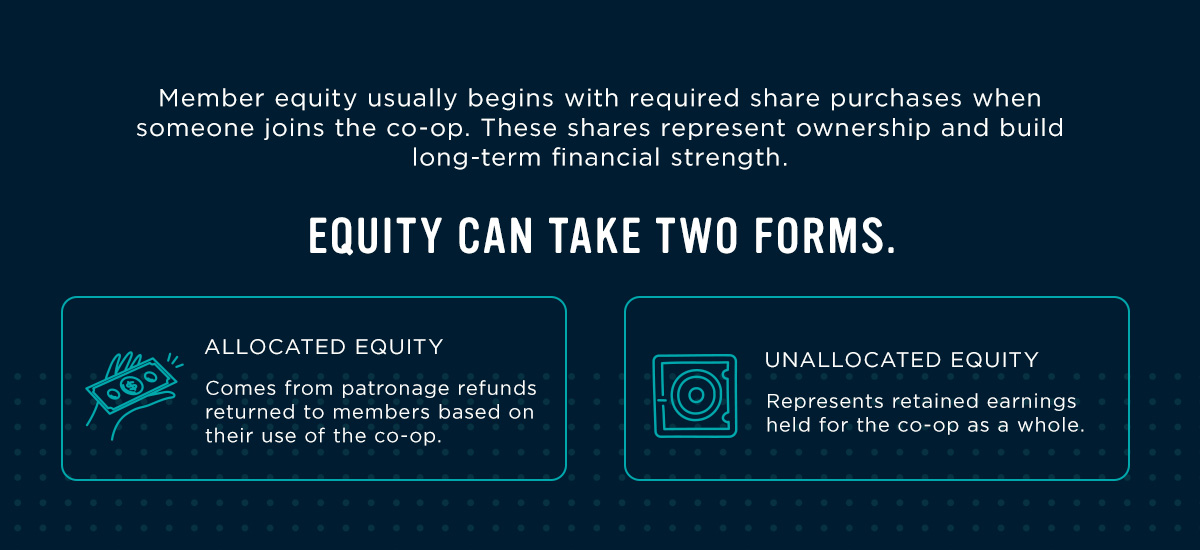

Member equity usually begins with required share purchases when someone joins the co-op. These shares represent ownership and build long-term financial strength. Equity can take two forms.

- Allocated equity comes from patronage refunds returned to members based on their use of the co-op.

- Unallocated equity represents retained earnings held for the co-op as a whole.

Voluntary member loans function differently. Members make these to the co‑op at a predetermined interest rate. They create a debt obligation but still demonstrate robust internal support — something lenders and grantmakers look for.

Together, these member-driven capital sources show that your co-op is viable, well‑supported and ready for outside investment.

Finding the Right Loan

Debt financing represents the most common form of external funding, typically through term loans for purchases or lines of credit for working capital.

While traditional banks hesitate to work with cooperative loans due to unfamiliarity with the ownership structure, a growing number of institutions specialize in lending to member-owned organizations. These mission-driven lenders understand your financial statements, value social mission alongside financial performance and frequently offer more flexible terms than conventional banks.

Securing Non-Dilutive Capital Through Grant Funding

Grant funding provides capital that doesn’t require repayment or dilute ownership — making it highly attractive but competitive. Government agencies and foundations commonly award grants to organizations that serve specific social or community needs.

Grants for cooperatives are typically available for specific projects or startup phases rather than general operating expenses. These cooperative grants require detailed applications showing community impact and organizational capacity, but provide valuable non-dilutive capital.

A Closer Look at Debt Financing

Since debt financing represents the primary external funding source for most member-owned organizations, understanding where to direct your efforts makes the difference between frustrating rejections and successful partnerships.

The lending landscape offers distinct options. Targeting lenders who understand your model empowers you to shift from justifying your structure to showcasing your strengths.

- Traditional commercial banks: Often unfamiliar with this model and uncertain about evaluating member ownership structures. Traditional underwriting frameworks designed for conventional corporations don’t translate well to your financials, leading to denials even with strong fundamentals.

- Mission-driven lenders: Understand your financial statements and use social mission as an evaluation criterion. They recognize that financing cooperatives serves broader community development goals that align with their mandates, creating partnerships rather than transactional relationships.

- Community development financial institutions: Operate under a federal funding mandate to serve economically disadvantaged communities, frequently aligning with these development missions.

- Cooperative banks: Structured as member-owned institutions, bringing firsthand understanding of your governance model and operational approach.

- Credit unions: As member-owned institutions, they are often more willing to support other member-owned enterprises. Mission-driven financial institutions like National Cooperative Bank specialize in raising capital for cooperatives with tailored financing and technical assistance.

How to Become Funding-Ready

Preparation turns interested funders into committed partners. Three foundational elements determine your readiness and establish your viability.

- Comprehensive business plan: Your roadmap articulating mission, market opportunity, governance structure and financial projections.

- Professional financial statements: Your balance sheet, income statement and cash flow statement prepared to accounting standards.

- Compelling story: Description of your community impact, core values and team capability.

The Importance of a Solid Business Plan

A comprehensive business plan stands as the single most critical document for securing funding. Your plan must include your mission statement and core values, market analysis showing demand, member structure and governance explanations and detailed financial projections covering revenue, expenses and capital needs.

Building a solid foundation for your funding application starts with covering all foundational elements, thus strengthening every aspect of your funding strategy.

Financial Documents Lenders Want to See

Funders require professionally prepared core financial statements. Your balance sheet shows assets, liabilities and equity at a specific point. The income statement reveals revenue and expenses over a period, showing profitability or a path to achieve profitability. Your cash flow statement tracks money movement, proving you can meet obligations as they come due.

Professionally prepared financials signal credibility and organizational maturity while speeding the due diligence process.

Crafting Your Story and Pitch

Mission-driven funders invest in your story and team as much as your numbers. Articulate the problem you solve, the values driving your approach and the strength of your member base and leadership. Explain why this model specifically serves your community better than traditional structures. Your narrative should demonstrate community needs and your organization’s unique capacity to address them effectively.

Your Clear Path to a Funded and Thriving Organization

You’re closer to a fully funded, thriving organization than you may realize. Your work will come to fruition once you understand your capital options, prepare the appropriate documents and connect with mission‑aligned partners.

NCBA CLUSA is your essential partner as you complete your due diligence and strategic planning. As the primary voice for cooperatives, our advocacy work expands access to federal funding while our educational tools and community of experts help you move from planning to implementation.

Are you ready to take the next step? Explore our extensive resources or become a member to join the movement toward a more inclusive economy.

![]()