Context and Options for determining eligibility for Cooperative Membership in NCBA CLUSA International

By Margaret Lund [1]

Executive Summary

This paper seeks to inform NCBA CLUSA’s Board of Directors in its work of defining a “cooperative” for the purposes of eligibility for membership in the association. The paper sets historical and contemporary context, provides examples of how “cooperative enterprise” is defined, and expands on the defining factors of operation on a cooperative basis:

- Member Ownership The dual nature of members as both active users[2] and joint owners of the enterprise,

- Member Control Democratic control of the enterprise by the membership, and

- Member Benefit Operation at-cost with surplus reinvested in the enterprise or distributed among members in proportion to use.

Finally, this paper proposes that for a cooperative business to be eligible for Cooperative Membership in NCBA CLUSA, it must:

First,

- Be incorporated under a state statute with clearly articulated requirements that adhere to traditional cooperative definitions of operation on a cooperative basis as stated above; OR

- Be incorporated under another state statute and demonstrate through articles, bylaws and other operational documents such as annual reports, meeting minutes, and organizational membership that the firm is both substantially structured in and operates on a cooperative basis in keeping with the above definitions; and

Second,

- Affirm its support of the Cooperative Identity, as defined by the International Cooperative Alliance (ICA), and the defining factors of operation in a cooperative manner as stated above.

In determining whether a firm substantially “operates on a cooperative basis,” staff of NCBA CLUSA will review the legal documents, operational policies, and other materials provided and consider the defining factors stated above. If any of these three elements is unclear, staff will have a checklist of questions for applicants that will invite them to articulate the ways in which their enterprise operationalizes the foundational elements of the ICA Cooperative Identity in its governance structure, operation, and practice. Conducted in a posture of inquiry rather than judgement, such a process will also help NCBA CLUSA to better understand ways in which cooperatives can serve new constituencies and purposes, explore priorities for legislative advocacy, and help potential members to better understand what structures and practices are necessary for cooperative operation and why these provisions support the impact and success of cooperative enterprise. Staff would periodically report to the NCBA CLUSA Governance Committee, providing an opportunity for further clarification, conversation, and dialog as we advance our vision and mission.

Introduction

The following paper is a description of contemporary U.S. cooperative thought and practice of the foundational question “What Counts as A Cooperative?” It is based upon interviews with 14 cooperative leaders from across sectors as well as supplemental written materials. Particular attention is paid to those recent practices (LLCs, Limited Cooperative Associations, community investment, nonprofit cooperative incubators) that appear to push the boundaries of what has been commonly understood as cooperative habits and norms, with intentional consideration paid to both practice (what is going on) as well as the thought and rationale behind it (that is, why?). Do such practices represent a potential dilution of our hard-fought brand and identity and therefore be resisted (or at least called out as Not A Cooperative)? Or alternately, are they a genuine and innovative attempt to adapt old ways to a new issue, population, or context, and therefore should be embraced (or at least guided)? Or both, or neither?

The purpose is to help guide the NCBA Board as it considers important questions of membership and dues structure. It may not be possible to articulate a definitive standard to meet all situations. However, following the lead of other cooperative bodies such as the International Cooperative Alliance, it would likely be possible to implement a membership process that is both forward-looking and inclusive, while at the same time respectful of our unique historic strengths as a movement. Ideally this process would not be too cumbersome and would instead promote valuable conversations within both our existing and potential membership regarding what exactly it means to be a cooperative in 21st century America.

Context

THE COOPERATIVE IDEAL IN THE AMERICAN CONTEXT

To many observers, the United States appears an inauspicious ground to plant the seeds of cooperation. Iconically individualistic with the weakest communal social safety net of any industrialized nation, the U.S. does not seem at first glance to be a promising environment for the growth of shared enterprise. But, as with many things, the view depends on the perspective.

The concepts of mutuality and cooperation are deeply rooted in the different communities that now are part of the American experience. Many if not most of the Native American communities practiced forms of mutuality before the Europeans settled North America. The Iroquois Confederacy (Haudenosaum) is frequently cited as one of the world’s oldest examples of participatory democracy. And as Jessica Gordon Nembhard points out in Collective Courage, Black and African American communities brought with them and continue to practice mutualism and cooperation as a tactic for resilience and survival.

In their 2014 book The Citizen’s Share, Joseph Blasi, Richard Freeman and Douglas Kruse show that the idea of the widespread ownership of productive enterprises was a familiar concept to the generation that framed the U.S. constitution. Washington, Adams, Jefferson and Madison all believed that the best economic plan for their nascent country was for as many citizens as possible to own land, which at the time was the primary productive asset. Widespread ownership of wealth-producing resources was an idea that would set America apart from the Europe of the 18th century, where few owned much of anything. Political democracy—however imperfectly practiced— is also as much a part of the defining American character and story as rugged individualism ever was. We are familiar, as Americans, with democracy in a political context; we generally aspire to widespread ownership of assets. The challenge for us, as cooperators it seems, is to link these two foundationally American ideals into a single concept in the American mind, to extend our cherished ideals of democracy to the economic sphere. It is not that we don’t know how to cooperate; perhaps it’s just that we don’t know that we know.

NEITHER ONE NOR THE OTHER

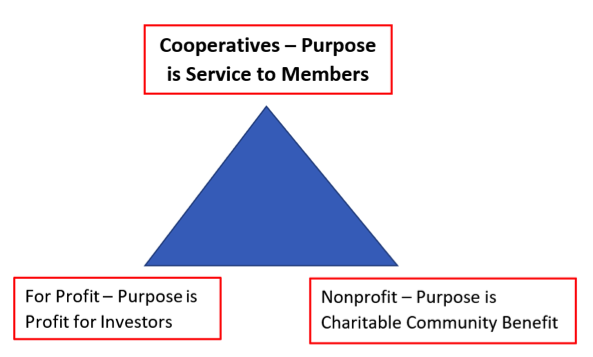

Commentators unfamiliar with cooperatives often describe them as “something in between,” an oddity existing somewhere on the continuum between two well-understood poles, that of a regular for-profit business and a non-profit charitable or beneficial organization.

Commentators unfamiliar with cooperatives often describe them as “something in between,” an oddity existing somewhere on the continuum between two well-understood poles, that of a regular for-profit business and a non-profit charitable or beneficial organization.

A more accurate depiction of the cooperative difference rather than a line, would be a triangle, where traditional investor-owned businesses would form one corner, 501(c )3 non-profit charities another, and the cooperative model would be a third kind of enterprise—in between in some ways, but also distinct with its own unique attributes and values that are not shared by either of the other alternatives. In this context, the traditional credit union motto of “Not for profit, not for charity, but for service (service to members, that is)” is an appropriate moniker for all kinds of cooperatives.

This distinction between a cooperatives and both its for-profit and non-profit peers is important in the context of this paper, as the deviations from traditional cooperative practice that we will examine typically are seen to emanate either from one of these alternate nodes or the other: in the case of LLCs or Limited Cooperative Associations (LCAs) cooperatives may be viewed as venturing “too close” to the for-profit model; in the more recent iterations of cooperatives founded by nonprofits as social enterprises, the cooperatives are sometimes seen as lacking independence from their parent organization, thus being “too close” to being a nonprofit.

Our purpose is not to pass judgement on whether something is a commendable business or a laudable social enterprise; they could well be both. But embracing some elements of fairness or democracy in a business structure while leaving others out, or organizing a business that also yields a good result for some defined community, do not of themselves, makes something a true cooperative. So, what does?

What sets cooperatives apart? Like their for-profit neighbors, cooperatives depend on a market context for their fruition. A “cooperative” entity with a single customer, for example, whether that be a government or NGO, would be unlikely to meet anyone’s definition of the Autonomy and Independence necessary to be a cooperative. And like their non-profit colleagues, cooperatives embody the pursuit of aspirational objectives that are distinct from, and much more comprehensive than, the simple return-on-investment metrics embraced by investor-owned firms.

One clear element that distinguishes cooperative enterprises from any other kind of enterprise is the institutional and foundational role of democracy in the cooperative structure and the attendant values of self-help, self-responsibility, equity and solidarity that the concept of democracy engenders. This is something that no other organizational entity shares; without democracy, you are something else, but not a co-op.

Another clear differentiator for cooperatives is the existence of an internationally accepted slate of clearly articulated shared values and principles. All nonprofit enterprises, and likely most for-profits as well, would argue that they also abide by values. What is unique about cooperatives is the fact that our values have clear and common language, and that they are shared by 2.6 million enterprises of all sizes in all sectors, on every continent except Antarctica. In this way, cooperatives are clearly something different, much more than just a convenient organizational business tactic; there has never been a United Nations International Year of the LLC (as there was for cooperatives in 2012), and there never will be, for good reason.

Who Defines Cooperatives Today?

ICA COOPERATIVE IDENTITY

The internationally accepted cooperative statement of identity, which includes the definition, principles and values of a cooperative, is a core defining characteristic of cooperative enterprise anywhere. Almost everyone interviewed mentioned the significant role that the cooperative principles play in cooperative identity for their sector. Nevertheless, whether the underlying core member of the cooperative identified first as a business enterprise (such as a farm or a small business)

rather as an individual did seem to make a difference in how centrally they viewed the cooperative values to their identity and character as enterprises.

While none of the cooperative leaders interviewed expressed a desire for themselves or anyone else to become the “Cooperative Identity police”, adherence to the ICA statement of cooperative identity as well as the internationally accepted cooperative principles and values were a vital differentiating feature for almost everyone interviewed. And interestingly, those practitioners involved in pushing the boundaries of some of the traditional cooperative structure in terms of the use of LCA statutes or LLCs were as committed to the values as anyone else.

Adherence to the cooperative identity may appear a rather vague standard to employ in trying to differentiate between something that is a true cooperative and something that is not. Fortunately, the International Cooperative Alliance has recently published a 120-page document of guidance[3] on what exactly it might mean to be a practitioner of cooperative identity, broken down by each of the seven principles with specific examples cited from various sectors. This document is an exceedingly useful standard to employ in the context of the conversation of what exactly it means to be a cooperative and may be of use to the NCBA if some sort of checklist or set of standards becomes part of the membership process.

STATE STATUTES

In many parts of the world, “what is a cooperative” is definitively established in statute, sometimes down to the minutia of minimum number of members, board composition and meeting dates. In the US, this job is done (or not done, as the case may be) by state statute. In regulated sectors such as credit unions and electric cooperatives, the variations may not be significant, and credit unions can actually choose to be regulated by the state of their incorporation or alternately on a federal basis. In other sectors, the world is a lot messier.

In many parts of the world, “what is a cooperative” is definitively established in statute, sometimes down to the minutia of minimum number of members, board composition and meeting dates. In the US, this job is done (or not done, as the case may be) by state statute. In regulated sectors such as credit unions and electric cooperatives, the variations may not be significant, and credit unions can actually choose to be regulated by the state of their incorporation or alternately on a federal basis. In other sectors, the world is a lot messier.

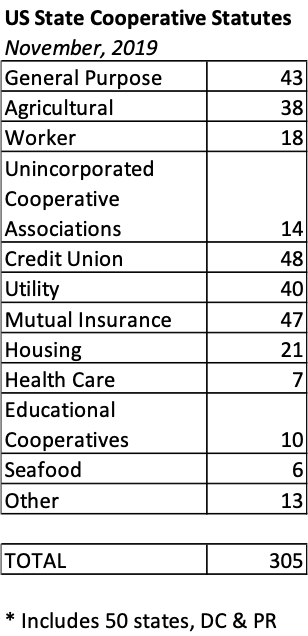

According to recent research by USDA[4], there are currently 305 different state cooperatives statutes in the US, including 43 general purpose statutes, 14 Limited Cooperative Association statutes and 6 that pertain solely to the seafood industry. Some of these statutes are succinct, clear, and broadly enabling of different kinds of enterprises (Minnesota’s and Wisconsin’s general-purpose statutes were noted); others (New York state was singled out) are seen by multiple interviewees as needlessly restrictive and arcane.

Many if not most of these statutes contain generally accepted elements of cooperative practice in their definitions (member patronage, democratic control, not-for-profit operations), but each has its own way of articulating it. Most, but not all, would be recognized as conforming to the International Cooperative Alliance (ICA) Statement of Cooperative Identity.

Several leaders interviewed for this paper noted the usefulness of state statutes in providing a readymade framework for protecting members’ rights, setting minimum meeting requirements, and making provision for reasonable access for members to corporate records and financial reports. Problems arise when a particular state statute fails to do this in a way that is meaningful for one or more group of cooperators. “Some states really don’t know what they are supposed to be doing” noted one interviewee with reason to know. Even within the confines of a decent state statute, there are others who would make the argument that part of the “autonomy and independence” principle of cooperation means that that an individual co-op should be free of local government control, and therefore able to incorporate their co-op in the way they see fit.

Thus, while state incorporation statutes play a useful definitional role in many cases, in more than a trivial number of instances, they do not: they are necessary to consider in our quest for definitional clarity perhaps, but not sufficient.

FEDERAL TAX TREATMENT

A second common way for enterprises to assert their status as a cooperative, is qualifying for federal Subchapter T tax treatment. An enterprise organized as an LLC, or a conventional corporation can establish its cooperative identity for the purposes of achieving the benefits of single taxation of surplus returned to members as patronage. Subchapter T is available to any corporation “operating on a cooperative basis” unless otherwise excluded. What it means to “operate on a cooperative basis” has been developed through case law and IRS ruling that consider ownership, control, and benefit.[5] While the case law and regulations are complex, three general themes from the seminal Puget Sound case generally run throughout: (1) limited return on capital; (2) democratic control of the members; and (3) allocation of margins based on patronage.[6]

Relying on subchapter T is problematic from a definitional perspective for several reasons. First, just like individual state legislatures, the IRS lacks sophisticated understanding of cooperative values and principles. Ceding definitional authority to an entity that does not particularly know or care about cooperatives very much is clearly problematic. Second, relying on guidance provided substantially through case law and IRS rulings needlessly injects an element of complexity and instability to the definition. And finally, while subchapter T tax treatment is highly beneficial for many cooperatives (and many would argue that the deductibility of patronage returns is a defining structural aspect of a cooperative), for other co-ops this tax status it is immaterial. Housing cooperatives, for example, purposefully operate at cost and rarely if ever generate surplus to be subject to tax. Even for some business cooperatives in some instances, subchapter T tax treatment may not be the most beneficial.[7] Thus again, while tax treatment might be a useful element in identifying as a cooperative an entity that is incorporated under an all-purpose statute, it is hardly exhaustive.

SECTOR ASSOCIATIONS OR APEX ORGANIZATIONS

The International Cooperative Alliance (ICA) itself has noted that membership eligibility in that organization can be “complicated” and requires an application and individual vetting process for new members. It relies on national apex organizations to some degree, but also has a membership process where applicants are required to submit a copy their organizational documents, most recent annual report, list of organizational affiliations and list of member societies (if relevant). Applicants must also fill out an application that requires affirmation of adherence and support for Statement of Cooperative Identity and has open-ended questions where applicants are asked to describe their organization and their reason for seeking membership. The ICA also makes provision for Full Members and Associate Members.

Other national apex organizations have wrestled to various degrees with this issue as well: Co-operatives and Mutuals Canada (CMC) also has a membership structure that differentiates between “Regular” and “Auxiliary” members, with Auxiliary members being individuals given honorary membership as well as cooperatives support organization such as educational institutions. A “Regular” member as defined in the bylaws is an organization “carry on business on a co-operative basis” that has been accepted for membership by the CMC, including by definition existing sectoral and regional associations. Cooperative Business New Zealand defines a cooperative as any organization (whatever the legal structure) that “ in the opinion of the Board, reasonably held, meet the definition of Co-operative as defined in the Constitution” which requires only that the “principal purpose” of the organization be to supply persons who are “members or shareholders” with some goods or services that allow them to pursue “common interests” and “derive benefits from their transactions” a definition so loose that it would likely not meet with the approval of any of the cooperative leaders interviewed for this paper.

In the U.S., specific cooperative sectors have also been pushed to more specifically define their membership in light of some of the innovations discussed in this paper. The National Council of Farmer Cooperatives, for example, allows LLCs or other entities into membership as long as the organization was “owned and controlled by farmers” and met the definition of eligibility to borrow from a bank for cooperatives.[8] The U.S. Federation of Worker Cooperatives requires member cooperatives to be a legal entity (not a collective), maintain legal ownership of the enterprise (that is, not be a subsidiary of a nonprofit or other organization), and demonstrate that worker-owners maintain a controlling interest in all decision-making on a 1 member, 1 vote basis. They also have a weighted voting structure where full cooperative members are given more votes in the organization than “democratic workplaces” that meet some of, but not all, requirements for being a worker-owned cooperative.

“Know Your Member” is a legal requirement of credit unions who must ensure that their approved field of membership is accurately followed. This would appear to be a sound operating principle for cooperative apex and sectoral organizations as well. Spending some time becoming familiar with the operations of members and potential members— particularly those whose practices are in some way not traditional—could be beneficial for all. It is arguably time well-spent if it help the overall organization to better understand the situations in which the concept of a “cooperative” is either being used in new and creative ways, or alternately, potentially mis-used.

Housing authority for the establishment of cooperative identity in a national sectoral body is appealing in many ways, but it also has its downsides. Some sectoral organizations are more active than others, and more importantly, there is no guarantee that various cooperative sectors in the U.S. will follow a common definition. Encouraging dialogue—both within and between sectors—rather than calling upon them to act as a regulatory body for the entire cooperative movement may be the optimal way to involve sectoral associations in this important discussion.

Ownership, Control and Benefit: The Practice

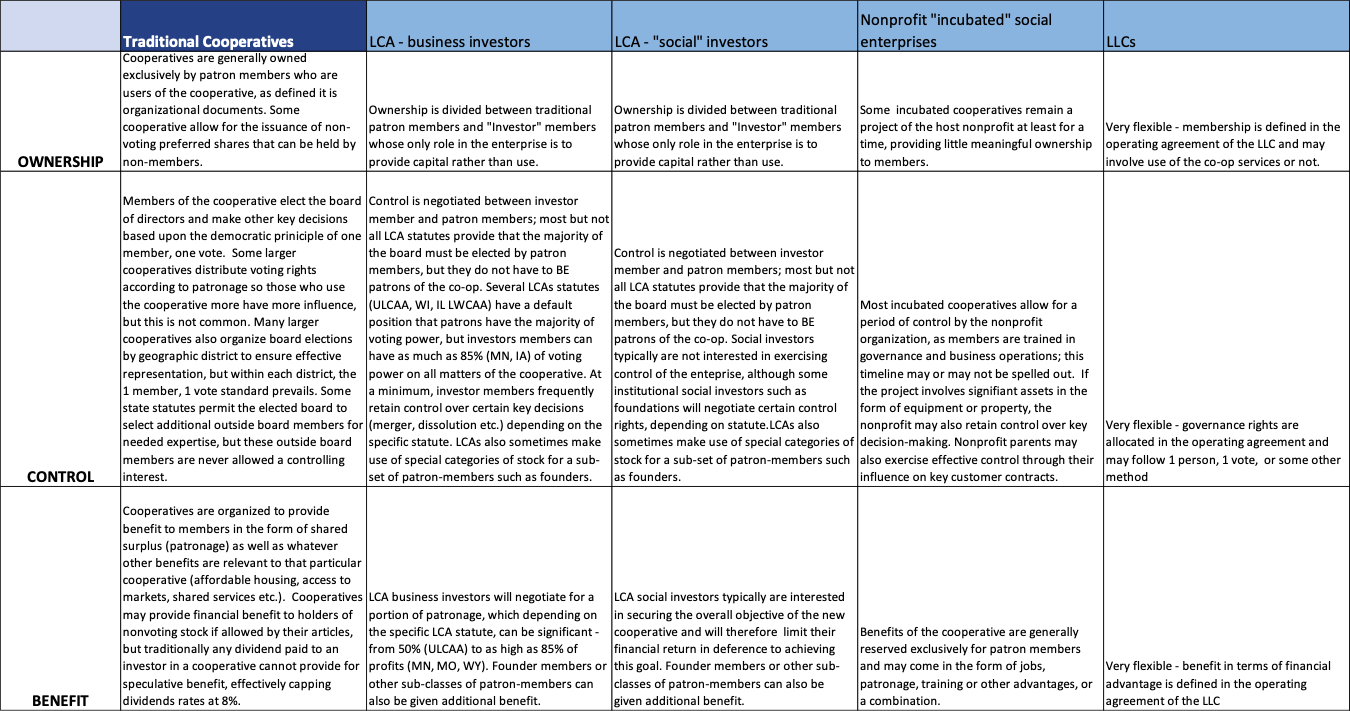

The defining attributes that were universally noted as defining characteristics of cooperatives by everyone across sectors and size of operations were Ownership, Control and Benefit by and for co-op members. Several people noted that actual function as a cooperative was at least as significant as legal structure or tax status. What you do and how you do it—consistently and clearly from year to year, is what defined cooperative practice. So how well do the new models of cooperation align with this foundational standard? First, some definitions:

TRADITIONAL COOPERATIVES

In a traditional cooperative, the answer to the questions “Who owns, who controls and who benefits from this enterprise?” is the same for all: the members. Traditional cooperatives are owned by members who democratically elect the board and otherwise exercise control over all decision-making for a stated purpose that is common and beneficial to all members. Surplus of operations, if any, is either repurposed for the good of members or distributed in an equitable fashion based upon the members’ patronage or use of the cooperative.

Within this definition, people commonly except certain variations. Credit unions serving low income communities, for example, can accept outside capital (secondary capital), but the amount is limited, owners of this capital receive no votes, and the use of outside capital must benefit the core members of the credit union. Other kinds of cooperatives, incorporation documents permitting, can issue dividend-paying shares to non-members; but these shares carry no votes, and dividends are limited to a non-speculative return typically 8% maximum. Many cooperatives bylaws allow for outside “expert” board members to be appointed by the elected board members. This practice, however, depends on state statute (Wisconsin’s general purpose statute for example, prohibits non-member directors) and such outside board members would typically always be in the minority.

The vast majority of states have specific statutes enabling the formation of credit union and electric cooperatives, and these statutes generally limit both ownership and governance (control) to members only. Perhaps because both of these sectors have a very broad membership base, even in these technical and highly regulated industries, members are seen by regulatory authorities to have sufficient ability to self-govern. Both sectors also invest heavily in providing accessible board training to all member co-ops, a laudable practice that could be copied more broadly.

NEW STRUCTURES OF COOPERATIVE PRACTICE

Limited Liability Company (LLC)

An LLC is a type of business structure that combines the pass-through taxation of a partnership with the limited liability of a corporation. Wyoming law first authorized LLCs in 1977, but LLC’s did not become common in other states until the 1990’s. LLCs provide enormous flexibility to distribute financial benefits and governance rights amongst the different parties involved and to change those distributions and parties as circumstances change. It is, remarked one observer, like “getting to write your own constitution.”

LLCs typically must distribute their profits and losses to owners every year, which makes them a difficult vehicle for enterprises with low income members (who are not able to easily absorb volatility or losses) or for those seeking to retain some assets within the enterprise itself for future use rather than distributing all gains annually to members. In the cooperative sphere, LLCs gained prominence for a period in the 1990’s and early 2000’s in the agriculture sector, and for a time appeared to be the preferred organizational form over standard cooperatives for attracting investment. LLCs have also been used in the past by social enterprise developers working with cooperatives of undocumented workers because gains can be reported to an individual tax ID number (TIN) instead of social security number. Organizations formed as LLCs can apply for and receive subchapter-T tax treatment by including in their organization documents the required cooperative elements of one member, one vote and distribution of gains according to patronage.

Limited Cooperative Associations (LCA)

Limited Cooperative Association statutes first came on the scene again in Wyoming about 2001. This new type of cooperative statute for the first time allowed for non-patron investor members and was intended to stem the “loss” of new cooperative ventures to the LLC model, while enhancing the ability of cooperatives to raise risk capital from outside investors. Because LCAs can be structured in ways that contradict some of the fundamental cooperative principles, their passage was controversial and remains so. Early LCA statutes such as Wyoming’s and Minnesota’s did a poor job of protecting member rights (under the Minnesota statute, as much as 85% of votes can be cast by investor members), but the subsequent Uniform Limited Cooperative Association Act (ULCAA) adopted in seven states and the District of Columbia does a better job at providing protections for patron members. There are, however, still elements permitted under this model statute do not strictly adhere to the international statement of cooperative identity.

While originally intended for agricultural cooperatives, in practice these statutes have not been heavily used, as large agricultural cooperatives have turned more to joint ventures and other such structures to meet their capital needs. It appears the most common usage of the LCA form has been either for capital-intensive social enterprises or for cooperatives in technology industries requiring growth capital. Investor members in different LCA co-ops have included small dollar, socially-motivated “community” investors, larger-scale philanthropic investors as well as sophisticated profit-motivated investors.

Social Enterprises and “Incubated” Cooperatives

The most recent development on the new cooperative model horizon is the emergence of various experiments in “incubating” cooperatives by a charitable nonprofit entity (usually low-income worker cooperatives but there is also earlier practice in this area in housing). The purported rationale for the initial control by the nonprofit is that new entrants into the business may not have all the skills and experience necessary to run a successful cooperative at the start, much less the capital, and therefore should be supported for a period with additional resources. These emerging projects around the country do not appear to be coordinated in any particular way, and vary enormously in their practice regarding whether the low income members involved actually own or control anything meaningful (presumably they do benefit from the mission of the co-op). Some well-run projects such as those developed by the Center for Family Life in New York City have a clear exit strategy for the nonprofit partner and plan for facilitating democratic decision-making and cooperative independence; other nonprofits demonstrate no such plan.

OBSERVATIONS AND COMPARISONS

The chart below outlines key differences between these new models and traditional cooperatives on the key functions of Ownership, Control and Benefit. Cooperative leaders did not fully agree on the degree to which these differences are meaningful, in either a good or bad way. Yet all had thoughtful observations on these core issues that are highlighted below:

Ownership

For most cooperative observers, the actual ownership of productive assets exclusively by and for the member-patrons of a cooperative is a key defining feature of a cooperative, and this ownership is evidenced by a financial ownership stake held by each member individually in the cooperative as a whole. Sometimes this stake can be substantial; at other times (in the credit union sector, for example) it is nominal.

The nonprofit end of the spectrum has pushed back on this requirement at times, arguing that low-income members should be exempt from making equity investments in the projects benefiting them. Yet worker cooperative leaders maintain that the existence of a real ownership stake, however modest, is a key defining feature of a business enterprise as opposed to a social program sponsored by a parent nonprofit.

In the affordable housing sector, experiment was made in the past with “leasehold” cooperatives made up of residents of low-income tax credit projects. Renters established co-ops and did not actually have effective ownership or control of anything, and for the most part these experiments were unsatisfactory to everyone. Much more successful were the dozens of HUD-sponsored limited equity housing cooperative projects organized in the 1970’s and 1980’s that allowed for a modest, but real, equity stake in the property by low-income residents. As one astute person has observed: “having a ‘sense’ of ownership is kind of like having a ‘sense’ of lunch instead of lunch itself—not very satisfying”.

On the issue of sharing ownership with non-patron investors, many cooperative leaders expressed discomfort at the practice of investor members in general, and in particular with the LCA statutes passed before the ULCAA was developed that are largely seen to cede significant ownership and control of cooperatives. In the words of one co-op leader “there is a nice clear other model for investor ownership, they should use it.”

The large agricultural cooperatives these statutes were intended to benefit have largely met their capital needs in other ways such as joint ventures. Old-fashioned cooperatives, it turned out, were beneficial after all, and farmers by and large are intensely proud to maintain their co-op as “farmer-owned.”

The actual benefit of these statutes has primarily been limited to the tech sector and to projects wishing to attract significant capital from socially motivated investors. Neither of these concerns is immaterial: if we want to be a cooperative movement that is open and accessible to all, then perhaps it is on today’s cooperative community to include business structures that can be adapted for 21st century industries. These structures may have capital needs that are distinctly different from the farmers cooperatives of the 1930’s that provide the base experience for so much of our current cooperative infrastructure. Many leaders working in cooperative development have been asking for years for more effective ways to bring nonprofit and community-based social investors into projects.

A final note regarding member-ownership is the concept of “stewardship”, which is important to many cooperative leaders. Some would argue that cooperative members have all of the rights of any business owner, including the right to liquidate and dispose of the co-op assets at any time for the benefit (profit) of current members; others see cooperative enterprises as being in a special position unlike that of a conventional investor-led business. Because the value of so many cooperatives have been built over time on the contributions of generations of members past, so this thinking goes, cooperative leaders are obligated to consider not only their own needs in decision-making, but also the needs of future generations of members. This point of view is widely held in the cooperative movement worldwide if not in the US. It effectively casts cooperative member-owners more as beneficiaries and stewards of a shared resource—temporary owners, not because they are going to sell the business, but because they are going to pass it on to their children and other members like them. In the U.S., the primary way we have to formally capture an impulse toward stewardship is the nonprofit institution; but as we see, nonprofit charity organizations such as 501(c)(3)’s have little experience with the democracy and member control that are so central to cooperatives. Providing ways, such as indivisible reserves, for cooperatives who chose to more effectively act as stewards of their enterprises would expand the benefit of cooperatives without diminishing ownership and control.

This is relevant to the issue of cooperative definition because indivisible reserves are a uniquely cooperative structural element that definitively separate cooperative enterprises from investor-owned corporations operating in similar industries.

Control

Member control is by far the most difficult of the cooperative triumvirate for outsiders, either nonprofits or investors, to understand and embrace.

Small scale social investors are generally not bothered by ceding control to the cooperative member board; offerings of non-voting preferred shares in well-known and trusted cooperatives such as CHS, Inc., Equal Exchange and Organic Valley routinely sell out in days. For larger investors seeking a stake in cooperatives, however, it is not uncommon for both profit-motivated and nonprofit investors in co-ops to negotiate key governance rights to overrule member control in certain situations, even if, in the case of nonprofits, this control would far exceed the control they would normally extend to a regular grantee. There is a lot of discomfort out there with member control by those who are unfamiliar with it, and this does not seem to be tempered by the fact that regular cooperative member routinely govern very large and successful entities like credit unions, utilities and agricultural co-ops. Members, on the other hand, appear to highly value member control. Board seats on successful cooperatives are coveted positions, and this is true across sectors.

Real, effective, democratic member control is also where the cooperative model really delivers on making real the values of equality, equity, self-help and self-responsibility; it is a foundational differentiating factor. Effective decision-making demands shared information, and authentically sharing information requires democratizing not only access to information, but also supporting members in understanding and using that data through widespread education and training (another cooperative principle).

The cooperatives that are most effective at institutionalizing these practices in under-resourced communities become, in effect, leadership generators. It is no accident that so many of the early leaders of the Civil Rights movement had early experiences with cooperatives. Scores of practitioners who have worked in effective grassroots cooperative development projects will attest to the power of authentic, member-led cooperatives to nurture leadership development in individuals, and generate social and economic transformation for under-resourced communities. It would be a shame if the need for capital from outsider organizations (or simply outsiders need to control something they don’t understand) were to undermine or obscure this valuable and unique attribute of cooperation. We should also not assume that outside investors will not share this perspective, once they understand it. One interviewee who embraces the LCA model actually prefers LCAs over LLCs because of how the LCA statutes clearly and definitively provides for member control.

It is also important to consider that control can be manifested in other ways besides governance. A social enterprise that has one effective customer (the parent nonprofit) is controlled by that entity, whether their representatives sit on the board or not. Similarly, an investor of significant enough size that the removal of their funds would threaten the enterprise also exerts effective control that is separate from governance rights. For low income credit unions that are permitted to take outside non-member capital (“secondary capital”) regulators and credit union boards ensure that these investments are not of a significant enough size to threaten member control.

Benefit

The first place most business observers look to define benefit is financial return. For cooperatives, return to investor members is an important concern. Traditional cooperative practice has limited return to non-member outside investors at a non-speculative rate (typically 8%). The need or desire to provide a more “risk-adjusted” (i.e. higher) return to investors is a driving argument behind all of the new investor-member cooperative forms (the members of a cooperative, of course, are not limited in the benefit they can accrue based upon their patronage).

Because cooperatives are not, in fact, investor-driven, they tend to define member benefit much more broadly than simple financial return. For worker cooperatives, benefit may mean a more flexible work schedule or influence on staffing plans. For a limited equity housing cooperative, the primary benefit for members is a safe and affordable place to live. For farmers and other businesses forming cooperatives, market access, lower prices for inputs and higher prices for outputs makes their home enterprises more profitable and thus provide a return in that manner. And for cooperatives cited above who see their work as “people development” as much as anything else, the cooperative’s democratic structure provides enormous benefit that is not available under ordinary for-profit or nonprofit models. Many cooperatives across sectors see the benefit they deliver to be multi-dimensional. Some electric co-ops, for example, state that they are in the “Quality of Life” business. Their job as such is not just to provide safe and accessible power, but to leverage their historic assets to provide additional benefits to rural communities like broadband service.

Even some active users of the LCA statutes will argue that the financial benefit given to investor-members is immaterial next to the more meaningful non-financial benefits that the cooperative delivers only to member-users, such as affordable housing for example. In this view, the actual financial return figure, whether it be 8% or something higher or something lower, is just not that important. What is important is for the investment not to be speculative, and for some overriding benefit of value to user-members to be delivered to those user-members.

Others would argue that cooperatives were invented so that people can organize to meet their common needs and aspirations, and that investors and patrons simply do not share a common need. Investors may believe in delivering the social benefit, but in a co-op that benefit should come through a self-help vehicle and not through the intervention of a third party who does not share the experience of those in need.

Conclusions and Recommendations

It is clear why some would view the emergence of the LLC option, LCA statutes or nonprofit social enterprise cooperative incubators as a threat to true cooperation; but it is also important to remember that they are not, in and of themselves, the enemy. They all are merely tactics put in place to meet an individual circumstance. While these derivations may in some cases be evidence of organizations trying to co-opt the “shine” of cooperation without doing the hard work of democracy, they may also be indicative of the ways in which our current cooperative statutes, support structures, or definitions are less than welcoming to a more widespread cooperative practice.

Clear standards and definitions are important not just for informing others, but also for delivering benefit: if we truly start looking like everyone else, we will have lost our point. Establishing some universal guidelines and guardrails will give guidance to those outside our current sphere who authentically wish to implement cooperative principles and nurture its benefits. Done carefully, building on our core competencies in the context of thoughtful discussion of the broad application of cooperative values and principles should work to expand our footprint in the world, not contract it.

Thus, this definitional exercise would ideally involve a simultaneous opening and closing our world: we don’t want to water down cooperative principles and practice, but we do want to better help others with shared needs and aspirations to see themselves in us. Are you watering us down or building us up? We should be able to answer that question, and act accordingly.

DEFINING A COOPERATIVE FOR MEMBERSHIP PURPOSES

There is some useful guidance from others that would be easy to draw on for the purpose of defining NCBA membership. For example, most state statutes other than LCAs encompass all the elements that would be generally seen to be foundational to cooperatives. We could identify the handful of state statutes that do not, and allow membership for any entity incorporated under an approved state statute to be automatically considered a cooperative. Similarly, it would be fairly easy and functional to consider any other entity with Subchapter T tax treatment designation to be “operating on a cooperative basis” while continuing to monitor court cases and IRS letter rulings (which NCBA would likely do anyway) to identify if IRS practice were to shift in a direction that seemed problematic. Requiring all members to at least nominally affirm adherence to and support of the international statement of cooperative identify as part of membership would also be a pretty easy thing to implement, and something most cooperatives would be proud to do.

The most difficult situations would be those entities formally structured as LLCs and LCAs that may or may not conform to the member ownership, control and benefit standard traditionally part of the cooperative identity. Because the actual practices of these entities vary so widely and have so many nuances, it would likely be difficult to articulate a single set of standards to define “operating on a cooperative basis” without excluding some worthy enterprise. Setting membership criteria for these enterprises might instead involve reviewing organizational documents, annual reports, minutes, and any membership affiliations such as membership in the relevant sector association—as the International Cooperative Alliance does—and asking applicants a set of specific questions about ownership, control and benefit. Taken together, these would yield a “preponderance of evidence” standard.

While we might not be able to publish a comprehensive set of rules to cover every situation, we certainly could give applicants the clear guidance that member ownership, control and benefit are the standards that need to be met. We could then give applicants the affirmative opportunity to show why their organization was also committed, both in structure and in practice, to these core principles. It need not be a judgmental or adversarial process, and might instead be part of a practice on the part of NCBA to “know your member.” Conducted in a posture of inquiry rather than judgement, such a process would also give the cooperative community the opportunity to better understand and learn from new practices, which also giving potential members perhaps some needed guidance on what changes would be necessary to make their enterprise a true cooperative.

Making a welcome place through auxiliary or associate membership for other entities that share our values but do not meet strict cooperative definitions would also be beneficial. There is no reason to turn away potential allies. If important, we could also make a category as New Zealand does, of “provisional” membership for enterprises with a stated objective of moving toward more complete member ownership and control.

OTHER POLICY THOUGHTS

Beyond a definitional exercise, there are also things that could be done by the movement in general policy and practice that would serve to discourage false uses of the cooperative name, while encouraging more broad application of authentic cooperative practice.

It is important to consider that these new cooperative entities and practices each emerged to some degree because of a void; in the absence of systemic direction or answers to their problem or need (capital for growth, a state statute that actually works for their kind of co-op etc.), these enterprises for better or worse, have created their own solution, and written their own constitution. People are innovating based on their individuals situations and understanding of what a cooperative is, sometimes to the good and sometimes not. If we are not able to provide them with definitive guidance or more flexible options or support, we can hardly complain when they don’t do what we want. The LCA statutes may have been a historic blip with highly limited application, and philanthropic interest in cooperatives or anything else is notoriously fickle. We don’t want to design our world around these entities, but we do want to listen to what they are telling us about the current climate and infrastructure for cooperative advancement as we want to see it, which is that perhaps it is not as robust as it needs to be.

[1] Margaret Lund, M Lund Associates, 612-750-1431.

[2] Member “use” of the enterprise is broadly defined here as including active purchase of products and services, use of facilities and services, and/or labor contributed, depending on the cooperative sector.

[3] “Guidance Notes to the Co-operative Principles” International Cooperative Alliance, 2015.

[4] Unpublished research, Meegan Moriarty, USDA

[5] See Donald Frederick, Income Tax Treatment of Cooperatives, pp. 13 et seq.

[6] Puget Sound Plywood, Inc. v. Commissioner, 44 T.C. 305, 308 (1965).

[7] One example is the Independent Natural Foods Retailers Association. When this purchasing cooperative started, they did not expect to be profitable for several years. As a new entity, they launched several different member programs simultaneously and did not want the burden of having to figure out and track potential member patronage on all of these different new lines of business when it was not yet clear which if any of them would be viable long term. Once the cooperative was more established with effective systems in place for tracking patronage, they changed their tax election to Subchapter T.

[8] NCFC Bylaws section 2(A)1.