![]()

In major cities, housing co-ops empower people with shared ownership and responsibility in their housing community. More than 1.5 million families, students and seniors in America benefit from the housing cooperative business model.

A housing co-op can be an apartment complex, a neighborhood of single-family homes, mobile home parks or student housing. Regardless of location, cooperative housing residents enjoy affordability, financial stability and collective ownership.

Members of housing cooperatives focus on the needs and interests of the group. Each resident is a shareholder in the building or land. They oversee and operate the co-op as a collective unit, not an individual real estate owner.

All residents contribute to decision-making in the community based on the seven cooperative principles, particularly a democratic ownership structure. Housing co-ops offer families limited liability, lower costs and a more empowered way to live as a community.

Key Facts About Housing Co-Ops in the United States

Cooperative housing gives residents a greater stake in their neighborhoods. Here are a few key facts about housing cooperatives in the U.S.:

- Co-op City in the Bronx, New York, is home to more than 15,000 families in 35 buildings, making it the largest housing cooperative in the world.

- Cooperative housing provides more than 1.5 million families with financially stable housing.

- More than 20 universities offer student housing co-ops near campus, reducing yearly room and board expenses by 50%.

- Cooperatives demonstrate resilience in the face of economic downturns, with the top 100 U.S. co-ops (including housing co-ops) generating an annual revenue of $324 billion, according to 2023 data.

What Is a Housing Co-Op?

A housing co-op is a member-based and member-operated organization that encourages affordable property ownership through shared resources and management. Each resident owns shares of the property and participates in its governance and obligations. This collective ownership ensures each member has an equal voice in the co-op’s decision-making process. Since housing co-ops are not designed for profit, they generate money through monthly fees from their members, which they then use to cover operating expenses.

Housing cooperatives are different from other housing types, like condominiums, where a person or entity owns a unit outright. They’re also different from rental properties, where the landlord or management company retains the right to make all decisions. Compared to single-family homes, housing co-ops offer a unique model of homeownership with shared responsibilities among members.

A few common types of housing cooperatives are:

- Limited-equity cooperatives (LECs): LECs keep housing affordable for future members by limiting resale profits when members decide to sell their shares. They are often used for low- and moderate-income housing and greatly benefit individuals and families looking for long-term, stable and affordable homeownership.

- Market-rate cooperatives: This type of housing co-op allows members to buy and/or sell shares at market prices, helping them earn equity from the sale. Market-rate cooperatives are common in higher-income or urban areas and are ideal for those seeking cooperative living with potential real estate appreciation.

- Leasing cooperatives: Also known as zero-equity co-ops, these are where the co-op leases the property rather than owns it. Members pay to live in the cooperative but don’t own shares of the property. They’re recommended for people seeking affordable housing but not interested in building equity.

- Resident-owned communities: These are housing neighborhoods collectively owned and managed by residents through a cooperative corporation. This model offers affordable housing to members and gives them democratic control over community decisions.

A BRIEF HISTORY OF HOUSING CO-OPS

Housing cooperatives first appeared in Germany in the mid-19th century and spread to the Scandinavian countries by the early 1900s. In the U.S., they began in the late 1800s in cities like New York and Chicago, offering the perks of homeownership without the responsibilities. It wasn’t until the end of World War I that their presence grew throughout the country.

At that time, the organizations generally fell into two categories. Many cooperatives catered to higher-income families to help them ensure neighborhood quality remained consistent. Unions and ethnic groups primarily organized the remainder to provide affordable housing solutions exclusively for their members in a tight post-war market.

In 1918, the Finnish Home Building Association established the first housing co-op adhering to the Rochdale Cooperative Principles in Brooklyn. Twenty-four other organizations followed suit, and many of those remain cooperatives today.

Large-scale co-ops began to organize after the New York State Limited Dividend Housing Companies Act of 1927, which provided substantial property tax relief and eminent domain rights for investors serving middle-income families. The Great Depression saw many high-income projects fail while those catering to lower-means families survived. Post World War II, the federal government began to join the cooperative effort by converting owned properties into member-run ones. These efforts continue to shape and influence housing co-op policies today.

The Importance of Housing Co-Ops

Housing cooperatives help improve the standard of living in their communities. They provide an affordable path to property ownership, boosting members’ pride. Thanks to their increased investment in the organization, members are more likely to participate in community activities that further benefit the neighborhood and its residents.

Cooperative housing benefits include:

- Affordable ownership: Housing cooperatives offer an affordable path to home ownership. They help make lower down payments possible and reduce closing costs

- Democratic control: Members gain a voice in democratic housing governance through their cooperatives. They also get a say in the co-op’s decisions, such as in budgeting and management, which is essential in promoting a sense of ownership.

- Community engagement: Housing co-ops operate on a shared ownership model, which encourages members to play an active role in the community and contribute to neighborhood well-being.

- Quality and stability: Members of housing cooperatives enjoy better quality housing and have more security because they are protected from arbitrary landlord decisions. Rental prices cover operating costs and reserves instead of maximizing profit, helping shield them from market fluctuations.

- Security of tenure: Affordable housing co-ops enable members to have a stable and permanent right to live in their space for as long as they follow the rules and pay their dues. They offer valuable protection from harassment from eviction.

- Personal and financial empowerment: Democratic housing governance, through housing co-ops, fosters a sense of empowerment among individuals. Below-market housing costs help free up income for other essentials and give people the means to afford a better life.

How Do Housing Co-Ops Work?

In today’s cooperative housing communities, residents buy shares to acquire a home, which remains an asset of the co-op. A proprietary lease or occupancy agreement gives the resident the right to occupy the home. Each member’s monthly payment contributes to the co-op’s property expenses.

Since residents share ownership of the co-op, taxes are also shared. Each member pays a small portion of the building’s taxes, while enjoying the same federal income tax deductions as a typical homeowner.

All housing co-op residents have a democratic say in which new members can join the community. Prospective residents undergo an extensive evaluation process to ensure they are financially responsible and care about the co-op’s interests.

Housing Co-Op Examples

Housing cooperatives can include many different types of residences or serve specific purposes, such as senior living. Membership is often selective — current owners want assurance that incoming residents share the co-op’s values and have the financial means to meet obligations.

Modern cooperatives generally fall into one of three types, including:

- Market-rate cooperatives: Market demand determines membership share prices. Much like traditional single-family homes, the price may increase or decrease, affecting the joining cost. These units often target middle- to high-income members.

- Leasing cooperatives: This co-op type, also called zero-equity, is similar to renting. The cooperative leases the property rather than owning it but may be able to buy it if the current owner decides to sell in the future. Under this arrangement, investor-owners can fix the share price or allow for annual adjustments.

- Limited-equity cooperatives (LECs): These organizations limit the price of membership shares during sales. Often, the restrictions produce lower interest rates on loans and taxes. The controls ensure affordable housing solutions for families who need them most.

In addition to Co-op City in the Bronx, well-known housing co-op examples include:

- Northern California Land Trust in Berkeley, California

- William Penn House Cooperative in Philadelphia

- Village Cooperative of Century Hills in North Richland Hills, Texas

Co-Op Associations in the Housing Sector

As economic development organizations push for more housing cooperatives, many U.S. and international associations work to advocate for and promote cooperatives, such as:

- National Association of Housing Cooperatives

- Resident Owned Communities, ROC USA®

- Co-operative Housing International

- International Co-operative Alliance

- Cooperatives for a Better World

The ABCs of Housing Co-Op Impact

Access

Housing co-ops are a proven way to expand access to affordable housing, particularly for limited-income residents. Because housing co-ops are one property, they can access a single underlying mortgage. This means that housing cooperative units can be financed collectively, individually or through some combination of the two. Improvements and repairs can also be financed collectively through funds borrowed by the cooperative, rather than assessed individually to homeowners. Housing co-ops operate at cost, so buying power is leveraged and monthly carrying charges only increase if actual underlying expenses do. In this way, cooperative homeownership presents fewer risks to a household than conventional single-family homeownership, and offers more control than rental housing.

Business Sustainability

Cooperative housing, in particular LECs, is a stable and effective means of low-income housing, proving resilient in the face of economic cycles that often negatively affect real estate investments. In comprehensive studies, cooperatives performed equally or better than nonprofit housing, with better overall survival rates. Housing cooperatives were also found to have lower operating costs when compared to nonprofit-owned developments, yet they were also conservatively managed and well-reserved for future capital needs.

Community Commitment

As member-owners work together on issues of common concern, they generate both individual and communal benefits. Data show that LEC residents participate in neighborhood organizations more and live in neighborhoods longer compared with low-income renters. A survey of almost 500 buildings in NYC found higher levels of social capital in the co-ops than in any other form of affordable housing. Even within the same geographic neighborhoods, the housing cooperatives in the study were consistently found to have the safest, highest-quality housing, and resident participation in community groups was key to that finding.

Democratic Governance and Empowerment

As their democratically elected representative body, cooperative housing boards of directors have a much greater ability to make and enforce house rules than do tenants associations of renters or even condominium association boards. This democratic influence — and, ultimately, collective control over the details of one’s living situation — has proved meaningful, especially for low- and moderate-income residents for whom control or even influence over their housing situation is often quite limited.

Equity, Diversity and Inclusion

Affordable housing co-ops in the U.S. have a long history of providing access to high-quality homeownership for members of all races and ethnicities. The 30,000 units of affordable housing saved and reorganized as resident-owned cooperatives by the Urban Homestead Assistance Board (UHAB) in New York City, for example, serve almost exclusively Black and Latino households. Despite being lower-income households in some of the lowest income neighborhoods in New York City, these cooperative members govern some of the city’s most successful affordable housing projects, providing high-quality, affordable resident-controlled housing for decades.

Financial Security and Advancement

LECs limit the speculative gain that residents can make when selling their home, but they deliver other financial gains that increase financial security for co-op members. Because housing cooperatives operate at cost, residents always know that their monthly housing costs will be kept in check. Lower housing costs and shared risk together allow low- and moderate-income families to confidently shift funds to other areas, such as education. Increased stability enjoyed by co-op residents also plays a direct role in their financial well-being. It has been established by numerous studies that housing stability plays a clear role in educational achievement. Housing stability has also been linked directly to job tenure and success.

Growth

Housing cooperatives contribute to the growth and economic well-being of their neighborhood. LECs provide a bulwark against gentrification and displacement, allowing residents of modest means to remain in place, even as surrounding property values increase. This makes economic growth more equitable for everyone.

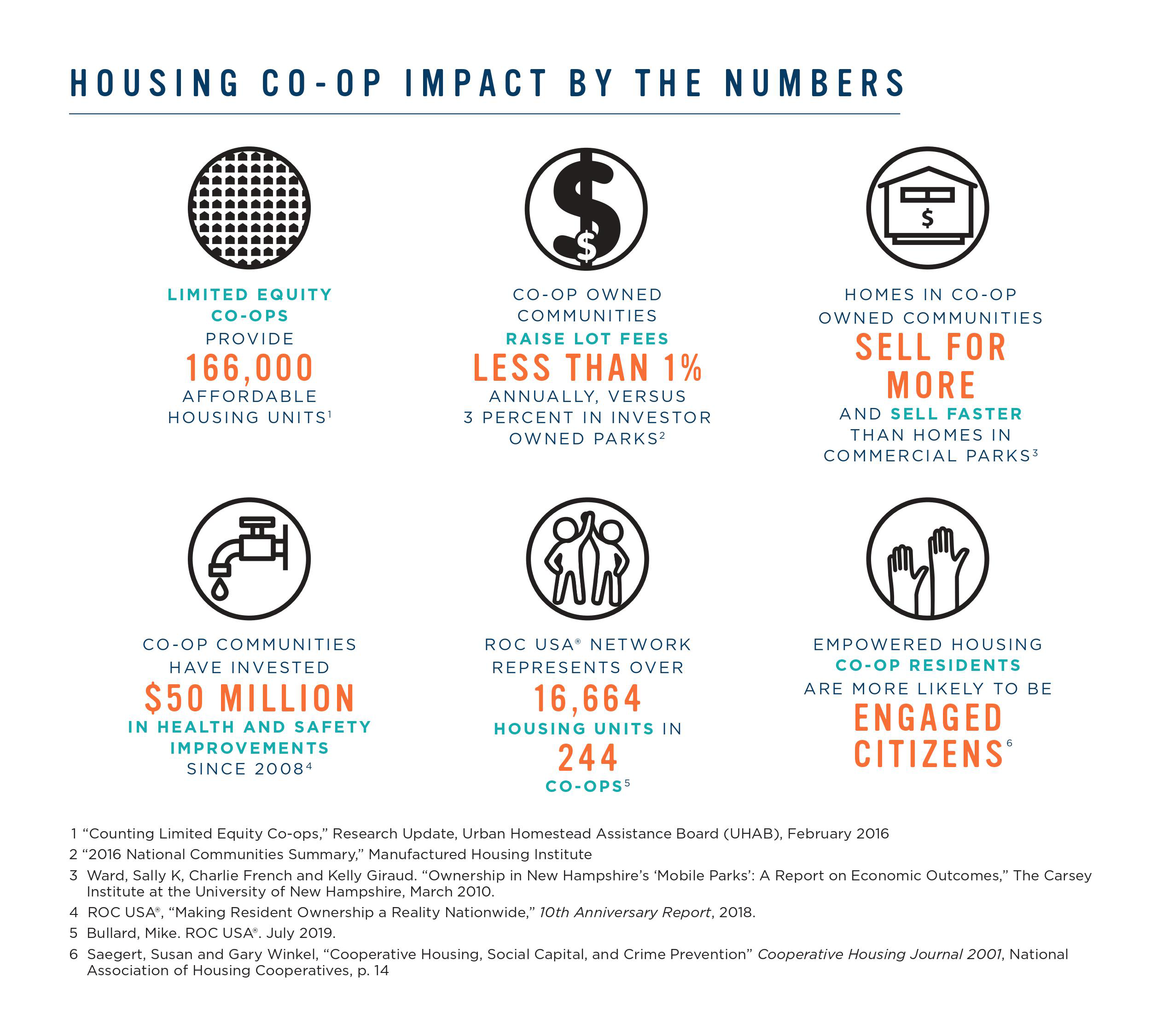

Case Study: ROC USA ®

A More Equitable, Inclusive, and Affordable Model for Ownership of Manufactured Homes

Manufactured, or “mobile,” home communities are an essential part of affordable housing in the U.S. There are about 37,000 such communities in the country, ranging in size from a couple of lots to several hundred. While people own their homes, they do not own the land beneath them, making them vulnerable to displacement. Not owning the land can leave them subject to substandard infrastructure and unreasonable rent prices, and with no say in community rules.

To combat exploitation, residents have banded together to form resident-owned communities (ROCs). Zoning laws typically prevent the purchase of individual parcels of land, so residents need to form an association to buy the property jointly.

Community ownership has significant advantages. For instance, in a long-term study by ROC USA®, co-ops raise lot fees an average of one percent annually, while commercial communities raise fees an average of three percent.

Cooperative communities also benefit homeowners when they sell their homes. Data from the Carsey Institute at the University of New Hampshire show manufactured homes in cooperatives sell for 16 percent more per square foot than comparable homes in comparable commercial communities. Homes in cooperatively owned communities also sell more quickly compared to homes in investor-owned communities. Since 2008, co-ops connected to ROC USA® have invested over $50 million in health and safety improvements, including water and sewer systems, roads, drainage and storm shelters.

After 25 years of co-op development work in New Hampshire by the Community Loan Fund, ROC USA® was formed in 2008 to scale co-op ownership nationwide. ROC USA® today represents 240 co-ops in 16 states. Nearly 16,000 homes have been secured to date, and that number is expected to double in the next ten years.

A Voice for Cooperative Enterprise

A better world starts with empowering people to contribute to shared prosperity. At NCBA CLUSA, we create collaborative partnerships through advocacy, public awareness and representation for the entire cooperative movement. This has been our sole mission for more than 100 years.

Be part of a globally recognized cooperative that advocates for its members’ interests. Join NCBA CLUSA today to participate actively in our ongoing work. If you’re interested in learning more about what we do, feel free to contact us online.