CONSUMER CO-OPS

The consumer cooperative model spans almost all business sectors, from a credit union to a CSA farm membership. When the customer has a say in and owns the products and services they use, it’s called a consumer cooperative. This democratic structure sets cooperatives apart from corporations that are led and owned by shareholders who are not necessarily using the product.

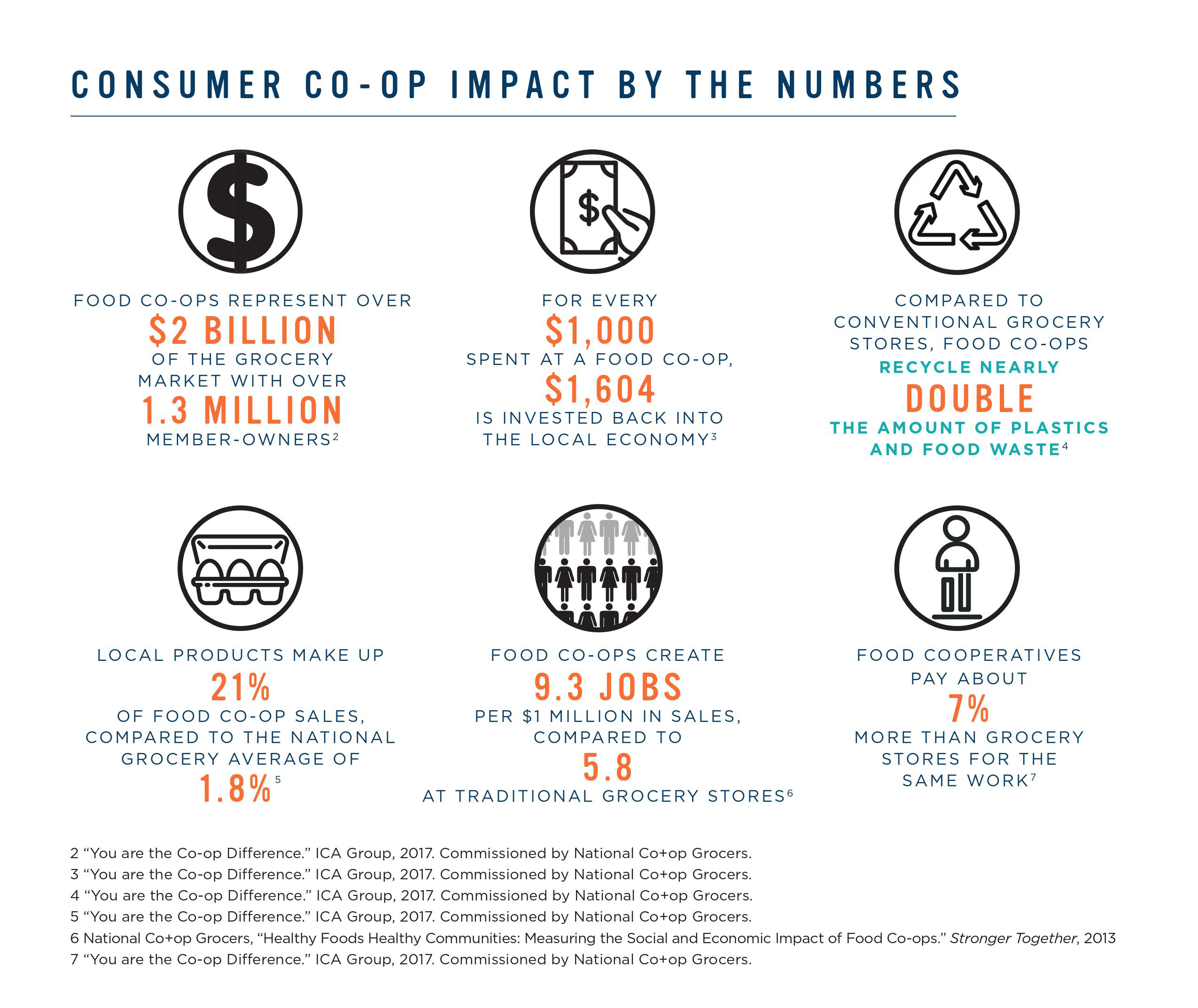

Learn more about the functions and benefits of consumer co-ops.

What Is a Consumer Co-Op?

A consumer co-op is a business owned by its customers, for the mutual benefit of its customers. The purpose of consumer cooperatives is to offer goods and services at the lowest cost to the customer-owners — in contrast to companies that serve the interests of stockholders.

A consumer co-op retains profits as capital with mutual ownership or invests the funds into the growth of the organization. The member-owners control the business and share a common goal to deliver quality products and services at low prices.

Co-ops operate under the guidance of the seven cooperative principles. The most important principle for a consumer cooperative is democratic member control, in which each member has one vote. This structure differs significantly from traditional businesses, which typically operate for profit and focus on achieving value for their investors.

Every member has the power to control the business by voting on leaders and deciding how to run the co-op. An elected board of directors is charged with hiring managers and monitoring the co-op’s progress toward financial and other goals. Each co-op holds regular membership meetings and maintains a set of bylaws or another organizing document.

In a consumer cooperative model, every member is a shareholder, so everyone’s voice is heard. Consumer co-ops focus on serving their customers, not turning a quick profit, and work within a mutually supportive economic model.

Why Join a Co-Op?

Consumer co-op membership gives power and freedom to businesses to grow at their own pace. Here are some of the benefits of joining a consumer cooperative:

Financial Benefits

Members may receive exclusive discounts on products and can benefit from any surplus, which is typically returned to members after being reinvested into the business. Members also negotiate the best prices to reduce fees and keep margins member-friendly instead of investor-driven.

Democratic Member Control

One of the main consumer cooperative advantages is that every member has an equal say in pivotal decisions, regardless of the amount of money they invest. Members can join committees, shape policies and engage in transparent board elections. All members also have a say in electing board members and choosing or running for leadership roles.

Community and Social Impact

Members of co-ops help improve their communities while increasing the business’s social impact. They can source locally, strengthening local businesses while reaping the benefits of regional suppliers. Co-ops can also create networking opportunities and build community-building events like fundraisers and classes.

Education and Resources

Co-op members benefit from the perspective of co-ops, which generally focuses on continuous learning and development for members. For example, members may enjoy financial coaching or fitness and nutrition classes, depending on the company’s goals.

Types of Consumer Co-Ops

Consumer cooperatives were first formed to fill a need for goods and services that were otherwise unavailable. These primarily centered around necessities.

Food

Food co-ops are typically local grocery stores owned by their members. These organizations collaborate with community farmers to offer fresh food and specialty options at lower prices. While nonmembers can purchase goods as well, members receive attractive discounts.

Specially structured food cooperatives also exist, such as preorder buying clubs. Under this arrangement, members place large, collective orders and receive them at a centralized point. Volunteers then sort and package each member’s order for pickup. Members can realize significant savings by eliminating the associated distribution and labor costs.

Housing

Housing co-ops are common in crowded metropolitan areas. They first appeared in the late 19th century in places like New York and Chicago to provide affordable housing solutions.

These organizations share the core cooperative values, but property ownership is collective. Members purchase equity shares in the co-op, which then issues a lease or approval of occupancy to the member. All members share in the property expenses and taxes through monthly dues, reducing their individual costs and risks.

How to Join a Consumer Cooperative

If you’re interested in reaping the co-op membership benefits, the right procedure can help you find the best cooperative for you. Follow these steps to become a member:

- Decide what you need: Are you looking to enjoy better costs on your favorite products, or do you need a service that could better the community? Decide on the goal of your desired co-op.

- Find a co-op you’re passionate about: Look for a co-op near you or within your field of interest.

- Evaluate your eligibility: Some industries may only be eligible for some individuals with the relevant location and skills. For example, those wanting to join a retail co-op may need relevant retail knowledge, while more general businesses may be open to all.

- Review the costs and perks: Find out what the one-time membership share is and gather information on ongoing dues. Consider whether the costs are within your budget and weigh whether the benefits, like discounts, are worth it.

- Apply: You’ll typically need to complete a membership application, pay a fee, and wait to get accepted or rejected.

- Participate: If your application is accepted and you’re eligible, you’ll need to be a participating member, which could mean tasks like attending meetings, voting and taking surveys.

NCBA CLUSA Supports Consumer Co-Ops

Over 65,000 cooperative enterprises operate across the U.S. At NCBA CLUSA, we provide a voice for these co-ops. Through resources and education, we create platforms for cooperatives to participate, lead and partner with others in the global community.

NCBA CLUSA and its members aim to advance development, advocacy, public awareness and thought leadership in the cooperative movement.

Interested in learning more? Read about the cooperative business model and NCBA CLUSA’s mission and vision. Feel free to contact us with any questions.

If you’re ready to build a better world and a more inclusive economy together, become a member today.

Linked sources:

- https://ncbaclusa.coop/resources/7-cooperative-principles/

- https://ncbaclusa.coop/resources/co-op-sectors/food-and-grocery-co-ops/

- https://ncbaclusa.coop/resources/7-cooperative-principles/

- https://ncbaclusa.coop/resources/co-op-sectors/housing-co-ops/

- https://ncbaclusa.coop/resources/

- https://ncbaclusa.coop/about-us/mission-and-values/

- https://ncbaclusa.coop/about-us/contact-us/

- https://ncbaclusa.coop/membership/join/